Both stories are true. Understanding why requires separating the cyclical from the structural, and the US market from the global one.

This article is written for procurement managers, supply chain professionals, and buyers across e-commerce, electronics, government, and industrial sectors who need a clear-eyed picture of where corrugated box manufacturing stands heading into 2026 — and what that means for sourcing decisions and packaging costs.

Key Takeaways

- The global corrugated board packaging market is valued at approximately $205.74B in 2026, growing at 3.73% CAGR through 2031

- US containerboard production fell 4% in full-year 2025 — a near-term warning signal worth watching

- Sustainability compliance and recyclability have shifted from brand values to procurement requirements

- Specialty segments — government spec, electronics-safe, and weatherized corrugated — are harder to substitute and carry more pricing stability

- Commodity producers face the most margin pressure; value-added and specialty configurations are better insulated from pricing volatility

The 2026 Corrugated Box Market: Size and Scale

What the Numbers Actually Say

The global corrugated board packaging market sits at approximately $198.34B in 2025, rising to $205.74B in 2026 per Mordor Intelligence, with $247.1B projected by 2031 at a 3.73% CAGR. Smithers puts the 2029 figure at $277.6B. The spread between forecasts reflects differences in scope (some include containerboard, some focus on converted boxes only), but the consensus clusters around low-to-mid single-digit annual growth globally.

The US picture tells a different short-term story. According to the American Forest & Paper Association (AF&PA):

- Q2 2025 containerboard production fell 5% year-over-year

- Q3 2025 fell another 3.1%

- Full-year 2025 production ended 4% below 2024 levels

- Q1 2026 operating rates settled at 91.6%, down from 92.3% the prior quarter, with box shipments off 1.9% year-over-year

These two narratives (global growth and US contraction) can coexist. Global growth is structural, driven by e-commerce adoption, urbanization, and sustainability mandates in emerging markets. The US decline is cyclical, shaped by tariff uncertainty, demand substitution, and a post-pandemic inventory correction still working its way through the supply chain.

The Cardboard Box Index

Those consecutive quarterly declines carry macroeconomic signal worth tracking. Former Federal Reserve Chair Alan Greenspan tracked corrugated box shipments as an informal economic barometer: boxes move before goods do. When manufacturers and retailers expect rising demand, they order more boxes. When they pull back, box orders often fall before broader economic indicators catch up.

According to Virginia Tech researchers, more than 75% of all non-durable goods ship in corrugated boxes, which makes shipment volume a credible leading indicator. The current readings — consecutive quarterly declines into Q1 2026 — warrant attention from anyone making forward purchasing decisions.

The Fibre Box Association notes corrugated packaging represents a $42B+ annual US industry accounting for roughly 40 billion packages per year. At that scale, corrugated packaging is foundational infrastructure for US goods movement.

Key Growth Opportunities Driving Corrugated Box Demand

E-Commerce: Still the Structural Engine

US retail e-commerce sales reached $1.19 trillion in 2024, representing 16.1% of total retail sales, up from 15.3% in 2023. Q1 2026 e-commerce came in at $326.7B, up 9.8% year-over-year — a clear indication that online retail isn't slowing.

For corrugated manufacturers, e-commerce remains the most durable demand driver. The caveat: large shippers are increasingly routing lightweight, non-fragile shipments into paper mailers rather than boxes. Amazon's 2023 US and Canada data showed **36% of shipments in corrugated boxes**, with mailers taking a growing share of the mix.

The net effect still favors corrugated for heavier, higher-value, and fragile shipments — but the lightweight segment is under real substitution pressure.

Food and Beverage, Electronics, and Industrial

Three verticals anchor demand beyond e-commerce:

- Food and beverage held over 37% of the corrugated boxes market in 2025 according to Grand View Research, driven by packaged food growth, food delivery, and cold-chain logistics requirements. This is the largest single end-use segment.

- Electronics and pharmaceutical sectors demand specialized configurations — anti-static, moisture-resistant, and high-crush-strength boxes — not just for protection but for regulatory compliance. These requirements make standard commodity boxes inadequate.

- Industrial manufacturing relies on corrugated for JIT packaging, bulk cargo containers (Gaylords), and heavy-duty triple-wall configurations that protect high-weight components.

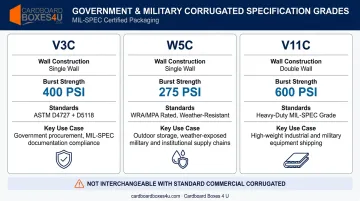

Government and Defense: Non-Cyclical by Design

Government, military, and aerospace procurement operates on contract cycles rather than economic sentiment. Buyers in this segment require corrugated products with documented compliance certifications and conformance to:

- ASTM D4727 — fiberboard material specification

- ASTM D5118 — finished container performance

- MIL-SPEC designations (V3c, W5c) for weatherized and heavy-duty configurations

Meeting those standards insulates compliant suppliers from the commodity price wars affecting the broader market.

Business Risks Facing Corrugated Box Manufacturers in 2026

Raw Material Cost Volatility

Kraft paper — liner and fluting medium — typically represents 70–80% of operating costs for corrugated manufacturers. This single input leaves the sector highly exposed to:

- Containerboard price fluctuations driven by global pulp markets

- Old corrugated container (OCC) fiber availability and recycling economics

- Energy costs tied to the energy-intensive nature of papermaking

When these variables move simultaneously in the wrong direction, margins compress fast, with limited ability to hedge unless manufacturers have locked in long-term supply contracts.

Overcapacity and Consolidation Pressure

The industry's response to weakening demand has been aggressive capacity rationalization:

- Smurfit Westrock announced reductions of over 500,000 tons of combined containerboard and CRB capacity in 2025

- Georgia-Pacific closed its Cedar Springs containerboard mill in 2025

- International Paper executed closures affecting more than 5,800 employees across a 20-month period through its string of facility shutdowns

- Overall, containerboard capacity shrank nearly 6% in 2025

This consolidation is reshaping competitive dynamics. Fewer, larger players now control a growing share of production, which will likely support pricing over time — but for smaller producers and industrial buyers, the near-term effect is tighter sourcing options and less pricing predictability.

Demand Substitution and Tariff Risk

Beyond supply-side consolidation, demand-side forces are creating additional headwinds for manufacturers:

- Mailer substitution is real, particularly for soft goods and lightweight apparel shipped through e-commerce channels. Paper mailers are gaining acceptance as a sustainable alternative, though corrugated remains dominant for heavier and fragile shipments

- Tariff volatility has suppressed export-linked packaging volume, with AF&PA data showing production for export fell nearly 12% in H1 2025. Fastmarkets projects box shipments declined 1.9% in 2025, with a recovery of 2.2% expected in 2026

Sustainability as a Competitive Edge

Recycling Credentials and Regulatory Tailwinds

The US cardboard recycling rate stood at 69–74% in 2024 according to updated AF&PA methodology — still among the highest recycling rates of any packaging material, and a clear procurement advantage for buyers with ESG commitments.

The regulatory environment is tilting purchasing decisions toward corrugated:

- Seven US states had packaging EPR (Extended Producer Responsibility) laws by 2025, with more in progress

- Single-use plastic bans at state and municipal levels are redirecting packaging spend toward fiber-based alternatives

- Corporate sustainability commitments across Fortune 500 companies now frequently specify recyclability thresholds that corrugated meets easily

For buyers sourcing from suppliers like Cardboard Boxes 4 U — whose corrugated products are recyclable and whose V3C and W5C grades meet WRA and MPA water resistance standards — this compliance is already built into the product specification. That matters when procurement teams need to document material standards for sustainability reporting.

Life Cycle Considerations

Compliance credentials tell part of the story. Life cycle assessments fill in the rest.

Corrugated performs well in single-use and short-supply-chain scenarios. Reusable plastic containers can outperform corrugated over many cycles in closed-loop systems with efficient return logistics. The procurement case for corrugated isn't that it always wins: it's that corrugated delivers strong environmental performance in most open-loop shipping scenarios, which describes the majority of commercial shipping.

Specialty Segments: Where Corrugated Demand Stays Resilient

The Commodity vs. Specialty Divide

The commodity corrugated market — standard RSC boxes for general e-commerce fulfillment — is the segment most exposed to price pressure, mailer substitution, and margin compression. The specialty market is different: buyers have specific performance or compliance requirements that standard boxes simply cannot meet, which makes substitution difficult and price sensitivity lower.

High-Resilience Specialty Categories

The specialty segments showing the most stable demand share a common trait: they require verified compliance, not just adequate protection.

**Government and military specification corrugated** requires conformance to ASTM D4727 (fiberboard material) and ASTM D5118 (finished container). Each grade designation has fixed performance thresholds: V3C (single wall, 400 PSI burst), W5C (single wall, 275 PSI burst, weather-resistant), and V11C (double wall, 600 PSI burst). None are interchangeable with standard commercial corrugated.

Cardboard Boxes 4 U maintains a catalog of 191 V3C ASTM D5118-compliant products plus dedicated W5C and V11C lines, with stock items available for immediate order and custom sizes on 10–14 day lead times.

Anti-static conductive packaging for electronic assemblies serves manufacturers who need ESD protection maintained across every handling touchpoint — from assembly through shipping to the end customer. Conductive black corrugated boxes integrate carbon-based materials into the board construction, providing protection against static discharge from personnel, equipment, and work surfaces. For electronics manufacturers, a single ESD event on the line can mean a scrapped assembly worth multiples of the packaging cost.

Suspension and retention packaging handles the high-value fragile goods segment where drop damage costs more than the packaging premium. Korrvu suspension packaging — carried by Cardboard Boxes 4 U — suspends products in the airspace between two layers of resilient film, maintaining protection through repeated drops and return shipments. This is the right solution for precision instruments, medical devices, and high-value electronics where foam alternatives aren't adequate.

Fanfold Corrugated: A Logistics Efficiency Play

Fanfold corrugated deserves attention from procurement teams optimizing inbound logistics costs. Because fanfold ships as accordion-folded bales rather than pre-formed boxes, two bales fit side-by-side in a standard trailer — achieving roughly twice the usable space per load compared to finished boxes.

For high-volume operations with CNC box-making equipment, fanfold also enables on-demand sizing, eliminating the need to stock dozens of finished box sizes and reducing both storage footprint and obsolescence risk. Operations running fanfold through in-house cutting equipment routinely report measurable reductions in inbound freight spend alongside lower SKU counts in the warehouse.

Profitability and Financial Outlook for 2026

Where Margins Stand

IBISWorld reports $94.7B in 2026 revenue for the US cardboard box and paperboard manufacturing sector, with 2.7% current-year growth despite overall sector pressures. McKinsey has documented that overcapacity, volatile input costs, and weak demand are compressing margins across the industry — but the pressure is not evenly distributed.

The margin story breaks along a clear line:

| Producer Type | Margin Outlook | Primary Drivers |

|---|---|---|

| Commodity RSC producers | Under pressure | Overcapacity, mailer substitution, raw material volatility |

| Specialty/compliance corrugated | More stable | Limited substitutability, compliance premiums, lower price sensitivity |

| Value-added (custom print, die-cut) | Protected | Differentiation, lower commodity exposure |

What This Means for Buyers and Procurement Teams

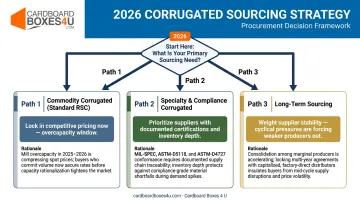

For buyers, the 2026 landscape creates a split market. Commodity corrugated is buyer-friendly right now — overcapacity has pushed pricing down, making this a reasonable window to negotiate standard RSC box contracts. Specialty and compliance-driven categories tell a different story: pricing holds firm because fewer suppliers can actually meet the specification.

E-commerce growth, expanding sustainability mandates, and emerging market demand keep the sector's structural outlook positive. The near-term US headwinds — tariff uncertainty, inventory correction, capacity rationalization — are cyclical, not structural.

Given that context, buyers have a clear split path for 2026:

- Commodity corrugated: Use current market conditions to lock in competitive pricing while capacity rationalization runs its course

- Specialty and compliance corrugated: Prioritize suppliers with documented compliance credentials and proven inventory depth

- Long-term sourcing: Weight supplier stability — cyclical pressures are already forcing weaker producers out

Frequently Asked Questions

What is the outlook for the corrugated boxes industry?

The long-term global outlook is positive — the market is projected to grow from roughly $205.74B in 2026 to $247.1B by 2031 at a 3.73% CAGR, driven by e-commerce, food and beverage demand, and sustainability mandates. Near-term US conditions are more challenging, with containerboard production down 4% in 2025 and shipments continuing to soften into Q1 2026.

Is the corrugated box business profitable?

Well-run operations remain profitable, though margins depend heavily on product mix. Specialty and value-added producers (government spec, custom print, anti-static) maintain healthier margins than commodity producers. Commodity-focused operations face the greatest pressure from current overcapacity and input cost volatility.

What are the biggest risks facing corrugated box manufacturers in 2026?

The three primary risks are: raw material cost volatility (kraft paper represents 70–80% of operating costs), demand substitution toward paper mailers for lightweight e-commerce shipments, and ongoing consolidation among major producers that is reshaping competitive dynamics and supply availability.

How does e-commerce growth affect corrugated box demand?

E-commerce remains a core structural demand driver, with US online retail sales reaching $1.19 trillion in 2024 and Q1 2026 e-commerce up 9.8% year-over-year. However, large shippers are routing lightweight shipments into mailers, partially offsetting box demand growth. Corrugated remains dominant for heavier, fragile, and higher-value shipments.

What is the recycling rate for corrugated cardboard in the US?

AF&PA's most recent data puts the US cardboard recycling rate at 69–74% in 2024 under a revised methodology. This remains one of the highest recycling rates of any packaging material and is a significant factor for buyers with ESG reporting requirements or sustainability procurement mandates.

What is the difference between standard and specialty corrugated packaging?

Standard corrugated (RSC boxes) serves general fulfillment with no specific performance certification. Specialty corrugated serves applications with defined compliance, protection, or performance requirements — including government/military spec grades (V3C, W5C, V11C), anti-static conductive boxes, weatherized WRA/MPA configurations, and suspension packaging like Korrvu systems. Commodity boxes cannot meet these requirements.